AI

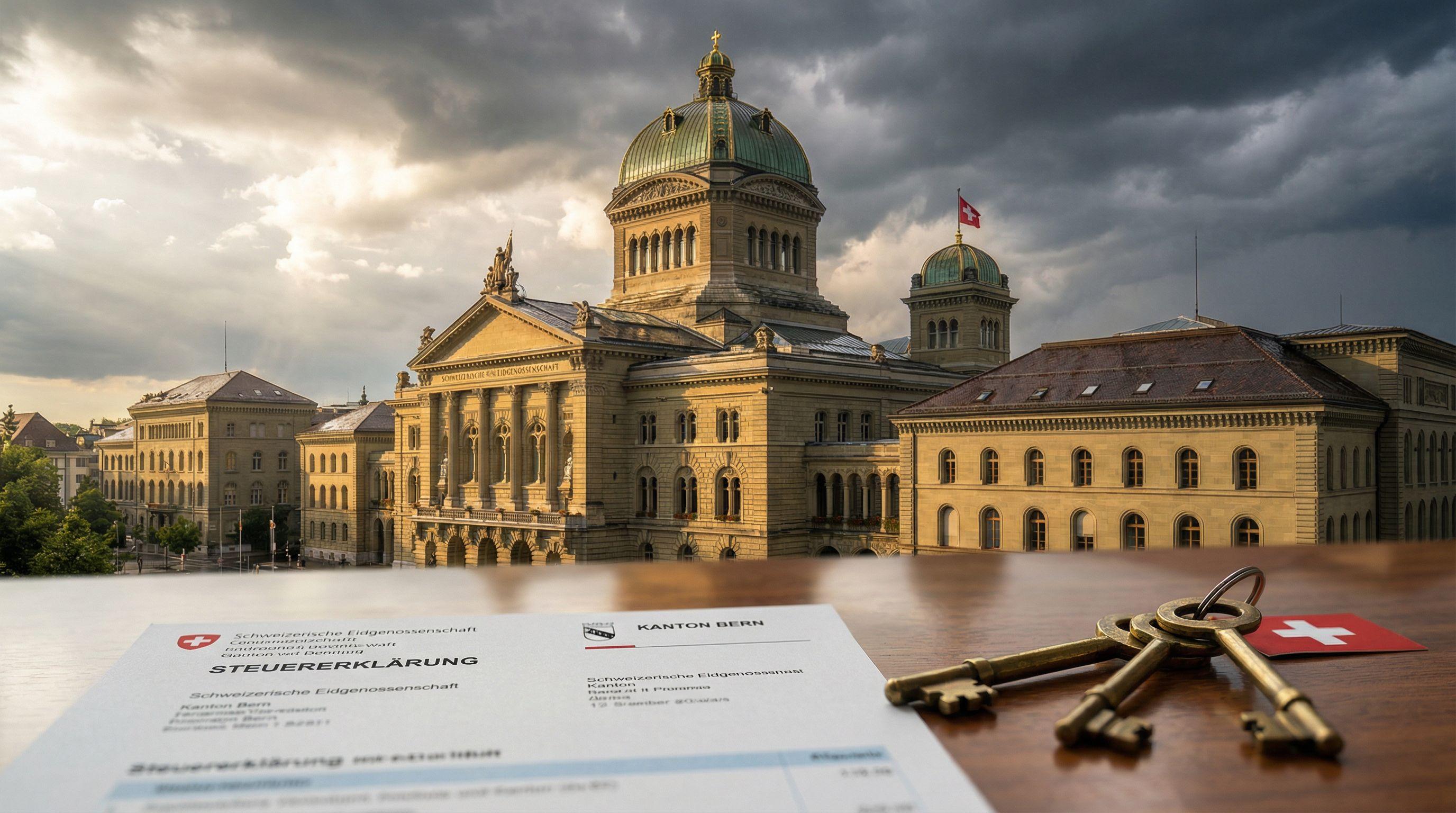

Swiss Parliament Ends Long Debate on Imputed Rent Abolition

After seven years of discussion, Switzerland's federal parliament reaches agreement on abolishing imputed rent system, marking significant change in property taxation.

AI

Generated IllustrationKey Takeaways

AI

- The Swiss federal parliament has reached an agreement to abolish the imputed rent system after seven years of debate.

- The abolition applies to both primary and secondary residences.

- Cantons will be permitted to introduce specific property taxes on secondary residences to offset lost revenue.

- Tax deductions for homeowners will be restricted to limit revenue loss at federal and cantonal levels.

- Resistance is expected, with a potential referendum requiring 50,000 signatures to challenge the decision.

By The Numbers

7 years

duration of legislative debate

50,000

signatures required

They Said

"After a stalemate last week, Switzerland’s federal parliament and upper house found a way forward this week on the abolition of imputed rent that both houses could agree on."