AI

Written with AI assistance•February 13, 2025•

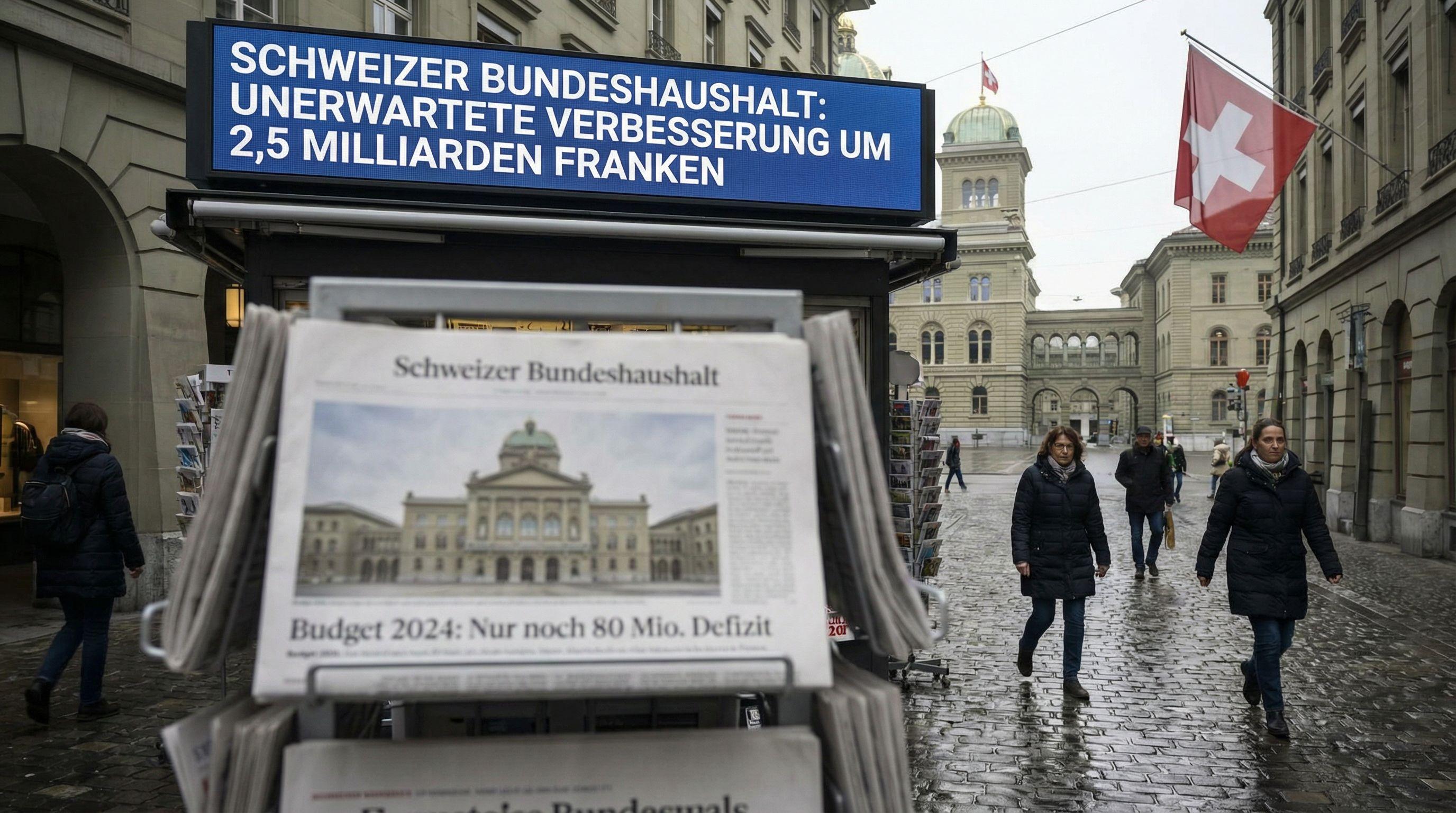

Switzerland's federal accounts for 2024 close with only CHF80 million deficit instead of expected CHF2.6 billion, marking first near-balanced budget since Covid pandemic.

"This means that no additional cuts are likely to be necessary for the 2026 budget."

"This increase in profits is a one-off, temporary phenomenon and therefore not sustainable."

Switzerland has defied grim fiscal forecasts, delivering a financial stunner that shatters expectations. Against a predicted shortfall of CHF 2.6 billion, the federal accounts for 2024 have closed with a negligible deficit of just CHF 80 million. This represents a staggering CHF 2.5 billion improvement, effectively wiping out the red ink that was expected to stain the government's ledger. For the first time since the global upheaval of the Covid-19 pandemic, the Swiss Confederation stands on the brink of a balanced budget, a feat that seemed impossible just twelve months ago.

Finance Minister Karin Keller-Sutter can breathe a sigh of relief as the provisional figures reveal a dramatic turnaround. While expenditure climbed by 4%, it was eclipsed by a robust 5.8% surge in revenue. The government attributes this massive deviation to a combination of fiscal discipline and unforeseen economic resilience. Extraordinary expenditures, such as the capital subsidy to the Swiss Federal Railways (SBB), were postponed, keeping cash in the vault. This isn't just a bookkeeping error in our favor; it is a testament to the volatility—and current vitality—of the Swiss economic engine.

Tax coffers have swelled, driven by a surge in receipts that outpaced conservative estimates by over CHF 1.2 billion. The driving force behind this windfall? A localized but powerful economic explosion in Canton Geneva. Energy and commodity trading giants, capitalizing on volatile global prices, have recorded exceptionally high profits, funneling unexpected billions into federal accounts. This sector alone is projected to pump an additional CHF 1.6 billion in income tax revenue into the system over the next three years.

However, the government is quick to label this a "temporary phenomenon." While the cash injection is welcome, it masks underlying structural realities. These commodity-driven spikes are volatile and non-recurring. Relying on them would be fiscal suicide. The additional income is currently earmarked to finance parliamentary decisions on increased spending—specifically for the armed forces and the compulsory contribution to Horizon Europe—but it acts as a bandage, not a cure. The message from Bern is clear: enjoy the liquidity now, but do not build the house on this shifting sand.

For years, the specter of Covid-19 debt has loomed over the Federal Palace, but 2024 marks the beginning of the payback. Because the economic situation allowed for a deficit of around CHF 500 million, and the actual result was far superior, the government has achieved a structural surplus of CHF 1.3 billion. This critical financial wedge will be driven directly into the mountain of pandemic-era liabilities.

Total federal debt has now dipped to CHF 26.8 billion—a reduction of CHF 400 million compared to the previous year. This is a pivotal moment for Swiss fiscal conservatism. While other nations continue to grapple with spiraling interest payments and ballooning deficits, Switzerland is actively deleveraging. The Federal Finance Administration (FFA) confirms that the ordinary financial balance sits at a healthy positive of CHF 817 million. This discipline provides the breathing room necessary to navigate an uncertain geopolitical landscape without the heavy anchor of unmanageable debt dragging down the Swiss franc.

The immediate horizon looks surprisingly clear. The government has announced that the 2026 budget is likely to be balanced without the need for additional, painful cuts—a direct result of the permanent spending reductions enacted in recent years. "No additional cuts are likely to be necessary for the 2026 budget," the government stated, signaling a brief pause in austerity measures. However, this stability is fragile and potentially deceptive.

Looking beyond 2026, the storm clouds gather again. Without the structural relief package currently under consultation, the federal budget faces a return to the red, with threatened deficits of around CHF 2 billion annually for 2027 and 2028. The current surplus is a reprieve, not a victory. The government warns against "exaggerated expectations," emphasizing that the Geneva commodity boom is a one-off event. To keep Switzerland's finances in the black for the long term, the proposed relief package remains a non-negotiable necessity. The battle for a balanced budget is won for today, but the war for long-term solvency continues.