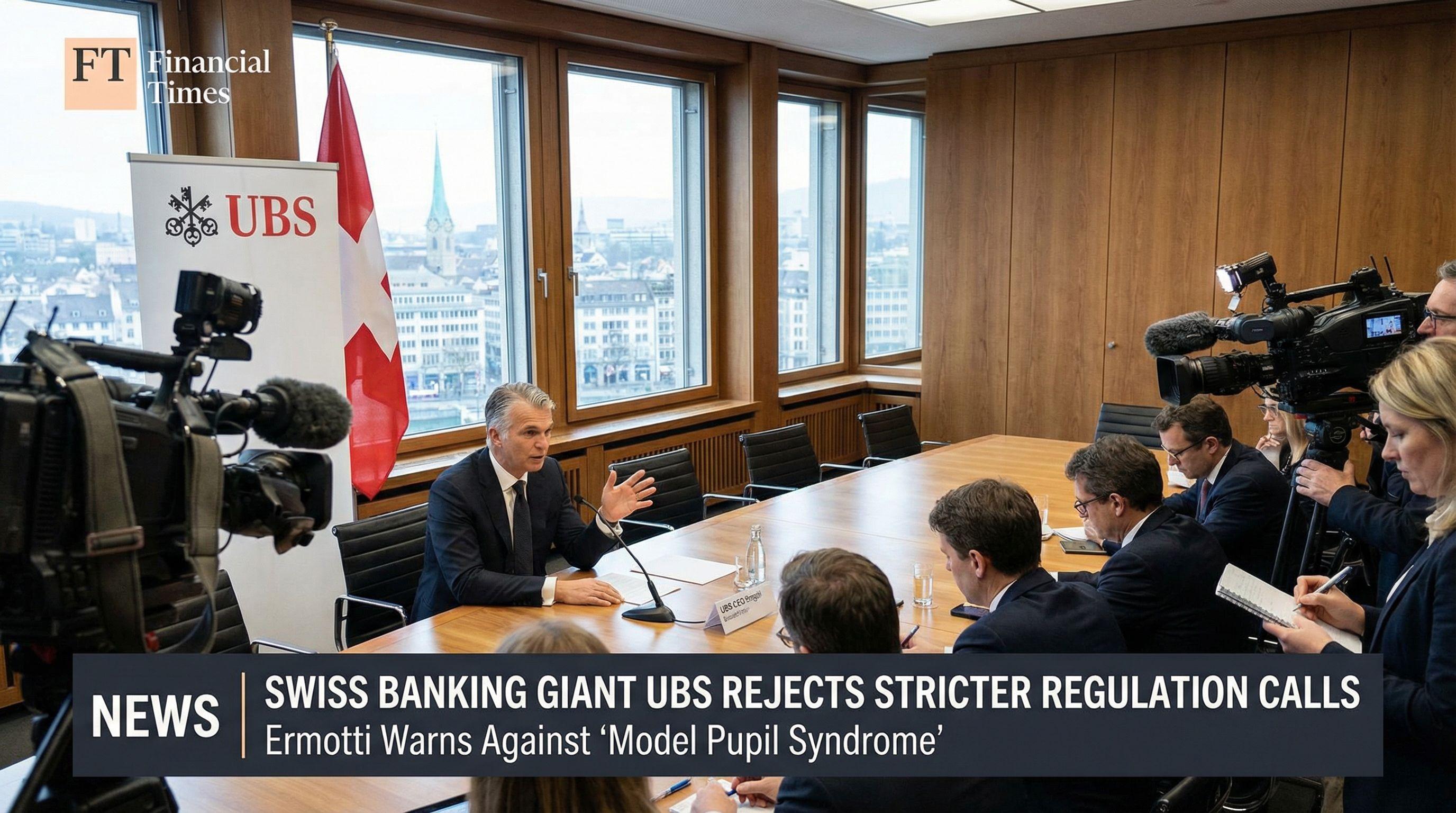

Switzerland stands on a regulatory precipice, and UBS CEO Sergio Ermotti is refusing to let the nation jump. In a defiant interview with Migros Magazine, the head of the banking giant issued a stark warning against what he terms "model pupil syndrome"—a tendency for Switzerland to self-impose stricter rules than its international rivals. Ermotti argues that while safety is paramount, over-regulation threatens to strangle the domestic financial center.

"We support many of the proposed measures, but they must be targeted and proportionate," Ermotti declared, drawing a line in the sand against blanket restrictions. His stance comes at a critical juncture as politicians and regulators debate the fallout of the Credit Suisse collapse. The CEO's message is clear: if Switzerland introduces draconian rules that other global financial hubs reject, it risks crippling its own competitiveness. This is not merely a defense of UBS; it is a strategic plea to maintain the nation's standing in a cutthroat global economy.