AI

Written with AI assistance•October 2, 2025•

New study reveals 53% of Swiss residents couldn't save in past six months despite 79% considering it important, with high fixed costs cited as main obstacle

"High fixed costs were cited particularly frequently as an obstacle."

"Respondents are most unsettled by uncertainties in the pension system and inadequate pensions or pension gaps."

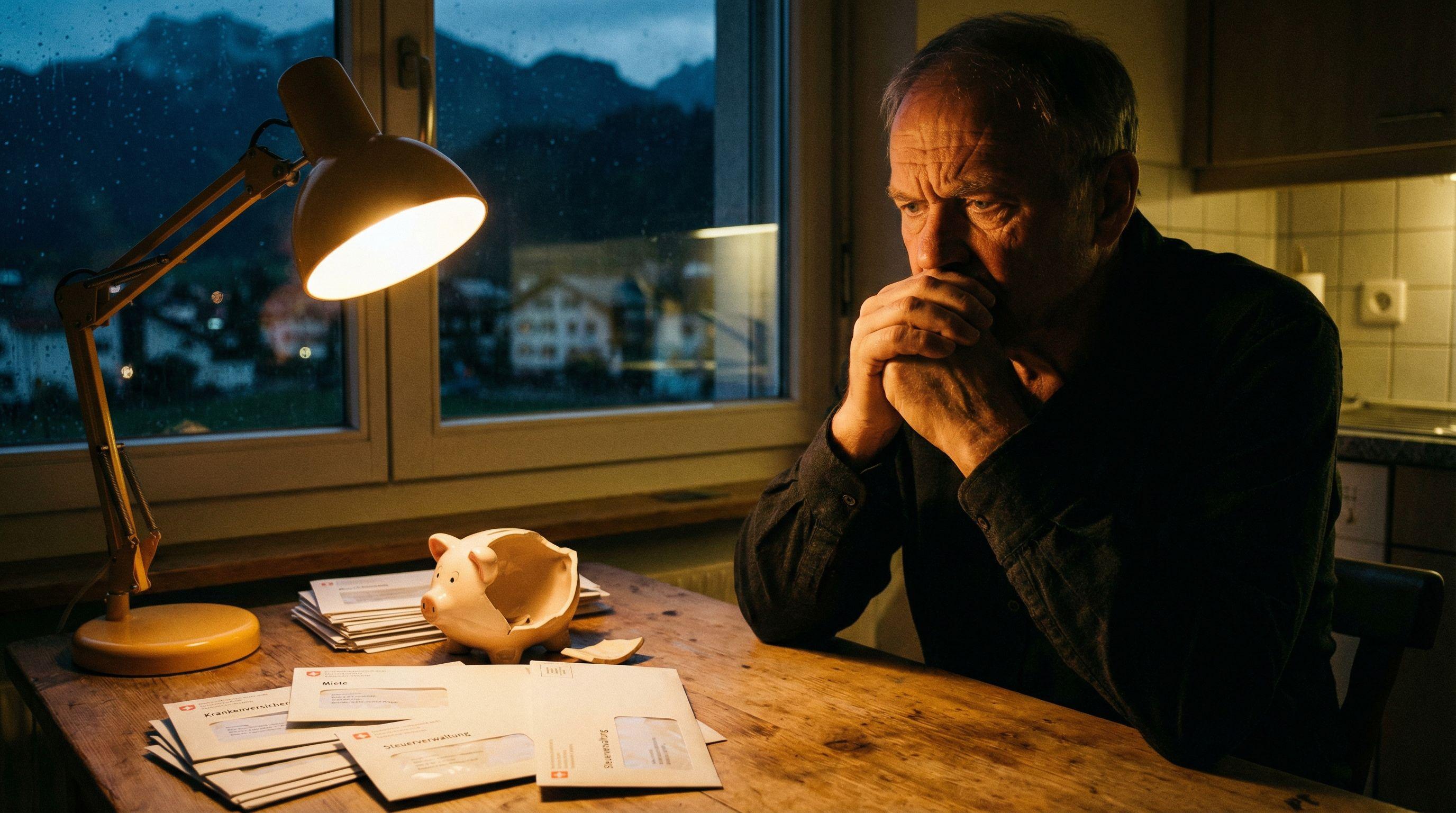

A staggering disconnect has emerged in the heart of Europe's financial powerhouse. While a resounding 79% of Swiss residents declare saving money a top priority, the harsh reality is that more than half—53%—have failed to put aside a single franc in the past six months. This alarming statistic, revealed in a comprehensive 2025 survey by Baloise and YouGov Switzerland involving over 2,000 residents, shatters the stereotype of the universally affluent Swiss household.

The gap between intent and execution is widening. Only 47% of the population managed to save anything at all, a figure that exposes the fragility of household finances across the cantons. This isn't a matter of apathy; it is a matter of impossibility. The desire to build a safety net is stronger than ever, driven by a need to prepare for unforeseen expenses, yet for the majority, the month lasts longer than the salary. As the cost of living crisis deepens, the Swiss tradition of thrift is colliding violently with economic reality, leaving millions with the will to save but without the means to do so.

The culprit behind this savings drought is undeniable: skyrocketing fixed costs are suffocating disposable income. Respondents to the Baloise study overwhelmingly cited non-negotiable expenses—likely rent and health insurance premiums—as the primary barrier preventing them from building wealth. The financial squeeze is so tight that even among the lucky 47% who do manage to save, the margins are razor-thin.

Nearly half of those who save are scraping together no more than CHF 1,000 per month. While this might sound substantial globally, in high-cost Switzerland, it represents a fragile buffer against financial shocks. The data reveals a defensive posture: the primary motivation for saving is no longer luxury or leisure, but security against the unexpected. Meanwhile, a generational divide is opening up, with the under-30 demographic aggressively prioritizing savings for residential property, fighting an uphill battle in a market that feels increasingly out of reach for the average earner.

Confidence in the long-term financial future of Swiss residents is plummeting. While a deceptive 57% of the population feels comfortable with their current situation, the outlook darkens dramatically when looking ahead. Only 44% of respondents express confidence in their long-term financial stability, a statistic that signals a looming crisis of faith in the Swiss pension system.

The dream of early retirement is rapidly becoming a mirage. Although over half of those surveyed fantasize about retiring early, a mere 11% are actively taking financial steps to make it happen. Even more telling, one-third of the population has resigned themselves to the fact that early retirement is completely unrealistic. The anxiety is palpable: respondents are deeply unsettled by pension gaps and systemic uncertainties. This disconnect between the dream of a secure, early exit from the workforce and the lack of concrete planning—or the financial ability to plan—suggests a rude awakening awaits a significant portion of the workforce.

Compounding the economic pressure is a critical failure in education: the Swiss are navigating this complex financial landscape blindfolded. A staggering 60% of respondents rate their own financial knowledge as mediocre at best. In an era of volatile markets and complex pension structures, this lack of literacy is a dangerous vulnerability.

The study highlights a systemic gap, with the majority of citizens calling for financial education to be mandatory in schools. Currently, financial acumen is not learned in the classroom but passed down informally through family and friends—a method that perpetuates inequality and misinformation. Without a robust understanding of how to manage money, invest, and optimize for tax efficiency, the Swiss population is fighting the cost-of-living battle with one hand tied behind their back. The consensus is clear: to secure the future, Switzerland must professionalize the way it teaches money management, moving from kitchen-table advice to structured educational reform.